CHICAGO, IL / ACCESSWIRE / September 20, 2023 / In an insightful recent article, Cboe Global Markets Inc. (BATS:CBOE) explores the rise of same-day expiry options - dubbed "0DTE options" - and their impact on volatility and institutional operations.

The first eye-catching observation in the article is the rise in popularity of these instruments. In 2016, 0DTE options made up just 5% of total SPX options volume. In 2023, this figure has risen to 43% as of this writing. In August of 2023, the figure rose to an average of a notable 50%, meaning if you picked an options contract, at random, from a pool of all the SPX options traded in August, you had a one out of two chance of picking out a 0DTE options contract.

Cboe writes: "As volumes have increased, so have concerns about the market impact of these products… Over the past year, commentators have blamed 0DTEs for everything from exacerbating intraday volatility to suppressing it, with estimates that market maker positions ranging from "record short" to "long $50bn" gamma in SPX alone."

The paradoxical nature of the claims suggests that there's a lack of consensus about the impact of 0DTEs on the market. The confusion likely arises because most operators do not have the data to arrive at fully accurate conclusions about the impact of 0DTEs. For options specialists like Cboe, that is not a problem.

Gamma Hedging Offers Insight Into Market Maker Dynamics

The first step in unraveling the truth is understanding gamma hedging. Gamma represents how the option delta changes as the underlying asset's price moves. For market makers who are managing their options positions, gamma indicates how much they need to adjust their delta hedge when the underlying asset shifts. Essentially, it shows how much they have to buy or sell S&P futures when the SPX index moves by 1%.

Market maker net gamma positioning has two key aspects to consider. First is the magnitude, which indicates the potential market impact of option hedging activity. The higher the magnitude, the greater the impact. Second is the sign of gamma. Being "long gamma" means market makers hedge in the opposite direction of market movements, potentially dampening market swings. Conversely, being "short gamma" means they hedge in the same direction as market movements, potentially intensifying market swings.

SPX 0DTE options are a focal point due to their high trading volume, averaging over 1.23 million contracts (equivalent to $500 billion notionally) daily in 2023. However, it's important to remember that volume alone doesn't equate to risk. What truly matters is the balance between buying and selling contracts, not just the total volume size. For instance, if 100,000 contracts trade for a specific strike, with 50,000 buyers and 50,000 sellers, market makers don't need to buy or sell S&P futures to hedge because the flow is perfectly balanced.

On average, market maker exposure to gamma is relatively small, ranging from $170 million to $670 million throughout the day. To put this in context, daily S&P futures trading amounts to around $400 billion. Therefore, potential hedging flows represent a minor portion, ranging from 0.04% to 0.17% of daily S&P futures liquidity. The balanced nature of 0DTE options trading, used by investors for various purposes, contributes to this stability.

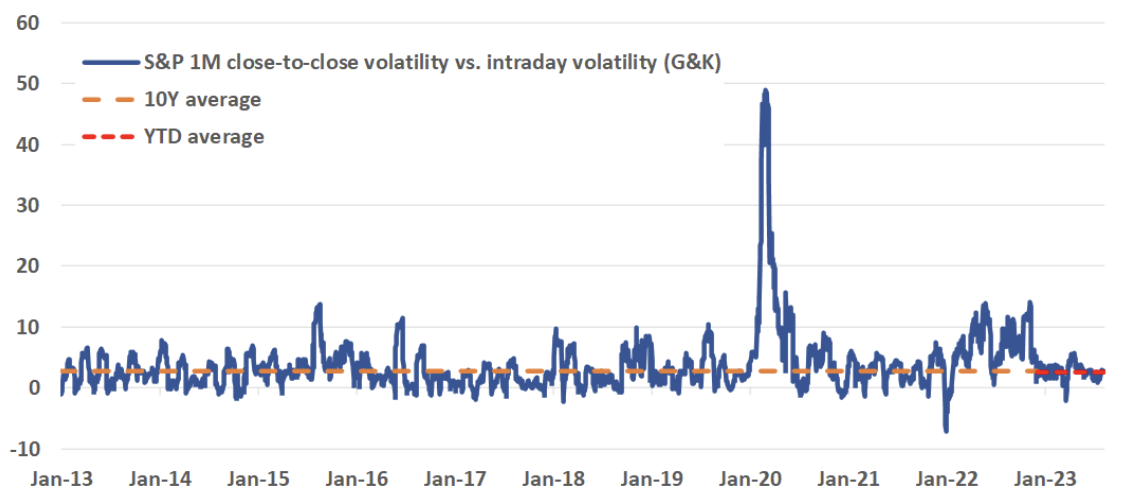

S&P Intraday Volatility: Has Anything Really Changed?

To assess the potential market impact of 0DTE options, another approach is to examine the SPX index's intraday behavior to check for any significant changes in intraday volatility since the rise of zero-day options.

The conclusion, as indicated in the chart, is that there hasn't been a noticeable impact. The difference between the S&P close-to-close realized volatility and intraday realized volatility remains consistent with historical averages. The year-to-date average spread of 2.7 volatility points matches the 10-year average.

Furthermore, when analyzing the intraday price movements of the SPX index to identify abrupt shifts possibly caused by substantial market maker hedging, there is no increase evident in the frequency of such gap movements over the past year since 0DTE trading became more prevalent.

More "Scary Headlines" Than "Truth"?

According to research by Cboe, the substantial notional volume in daily SPX 0DTE options trading has had minimal impact on market makers' actual exposure. The exposure ranges from 0.04% to 0.17% of daily S&P futures liquidity. Moreover, there is no noticeable market impact from 0DTE option trading, with intraday volatility and price patterns in line with historical averages. This stability is primarily due to the balanced nature of 0DTE trading, which serves a wide range of uses for both institutional and retail investors.

Read more here.

Featured Photo by Aditya Vyas on Unsplash

Contact:

Michele Ormont

[email protected]

SOURCE: Cboe Global Markets, Inc.